Investment Philosophy & Edge

Beyond Outdated Paradigms.The Institutional AI Advantage.

Traditional market exposure is insufficient in a world of episodic volatility, rapid regime shifts, and non-linear cross-asset correlations.

The Limits of Traditional Financial Theory

True alpha is defined by risk-reward ratios, volatility scaling, and tail-risk minimization.

For decades, the global asset management industry has relied on Modern Portfolio Theory (MPT) and the Efficient Market Hypothesis (EMH). These frameworks are structurally flawed, built on the assumption of rational market actors and normally distributed returns. In reality, these outdated models repeatedly fail during periods of systemic stress, liquidity contraction, and non-linear market shocks. The statistical reality is that the vast majority of active managers fail to outperform their benchmarks over extended horizons because they rely on static models in a dynamic world.

Furthermore, mainstream financial punditry remains disproportionately fixated on the single, flawed metric of pure benchmark outperformance in bull markets. At Qlumina, we recognize that absolute return generation cannot be measured by gross returns alone. Institutional capital preservation demands a holistic evaluation of performance. True alpha is defined by rigorous risk-reward ratios, volatility scaling, and the absolute minimization of tail risk. We do not optimize for raw momentum; we optimize for convexity, targeting returns with substantially lower volatility than public markets to ensure continuous capital resilience.

Non-linear market shocks

The framework is designed around stress, liquidity contraction, and changing cross-asset behavior.

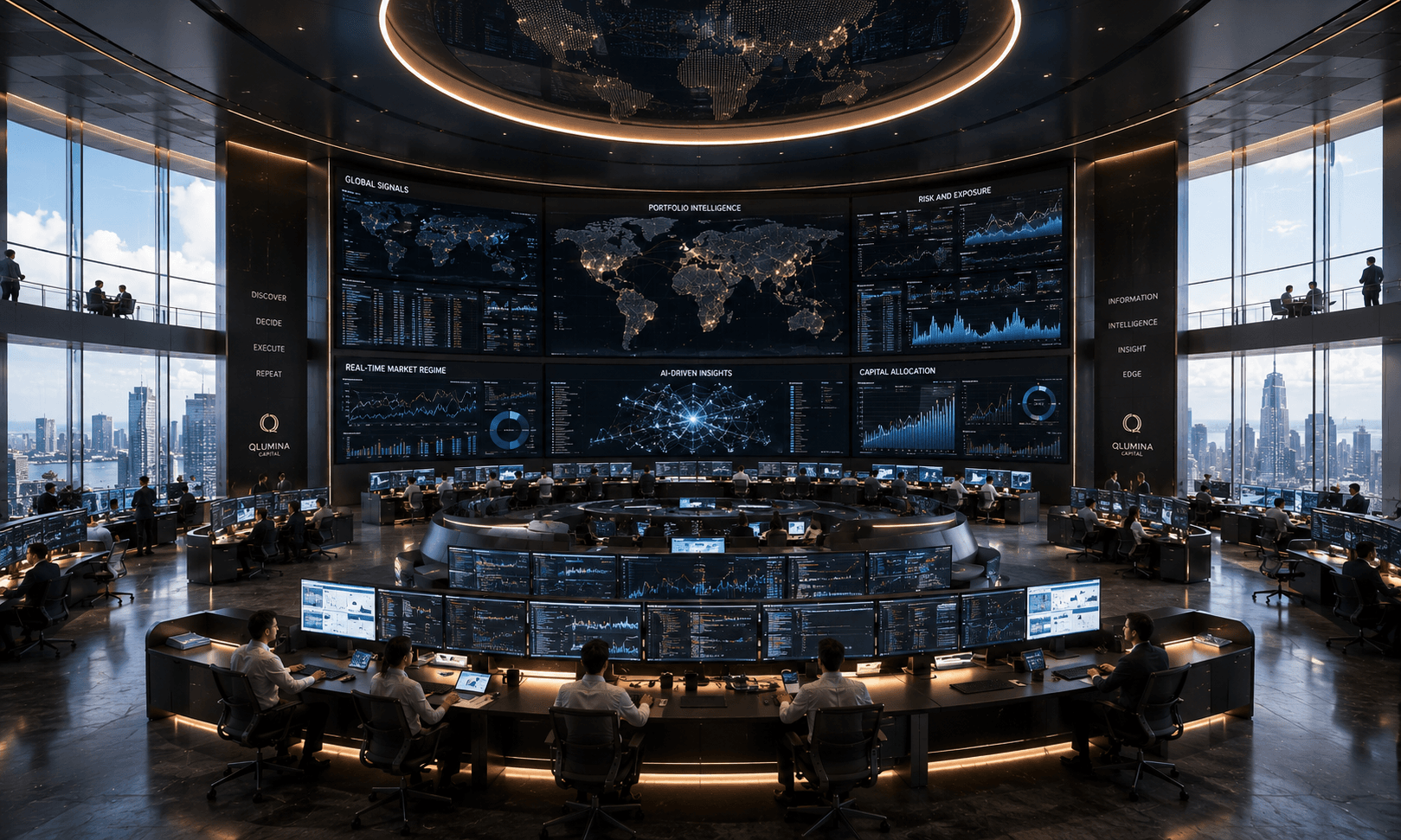

The Qlumina AI Core: Intelligence at the DNA Level

Our investment engine is 100% AI-native, combining two distinct but complementary technological frameworks.

Large Language Models (LLMs) for Financial Intelligence

Our proprietary infrastructure utilizes advanced LLMs for real-time market understanding, natural language processing of macro events, sentiment analysis, and the mapping of cross-asset knowledge graphs.

ML/DL Engine for Predictive Modeling

Our Deep Learning framework is trained on over 20 years of market data. It powers our predictive modeling, pattern recognition, and adaptive reinforcement learning algorithms, continuously identifying changing market regimes.

The 65-Agent Autonomous Ecosystem

Our human leadership is augmented by a continuously operating, 65-agent autonomous AI organization.

These agents perform billions of simulations and portfolio optimizations 24/7 across specialized departments:

Research & Strategy

12 AgentsGlobal macro, thematic research, and scenario modeling.

Data Engineering

10 AgentsData ingestion, feature pipelines, and quality control.

Backtesting & Robustness

8 AgentsSimulation, stress scenarios, and model validation.

Execution & Microstructure

8 AgentsOrder routing and slippage optimization.

Portfolio & Risk

10 AgentsAllocation engine, volatility, and tail risk control.

Finance, Compliance & Ops

8 AgentsNAV oversight and automated reporting.

Intelligent Portfolio Construction & The 10 Alpha Engines

Our unified portfolio construction is powered by 10 complementary, uncorrelated quantitative alpha engines.

Through our Intelligent Portfolio Construction framework, we take established, tier-one external managers and synthesize their strategies with our internal AI engines. Our AI algorithms optimize position sizing, enforce strict correlation parameters, and dynamically apply strategic leverage. This process takes fundamentally sound strategies and elevates them into a single, world-class, highly defensive institutional portfolio.

Capital preservation

Automated de-risking, human oversight, liquidity buffers, and infrastructure redundancy operate together.

Systematic and Multi-Layered Risk Management

Capital preservation is embedded at the code level through a rigorous, multi-tiered control architecture.

Autonomous AI Strategy & Portfolio Layers: Independent AI agents continuously learn and adapt, optimizing strategy parameters and detecting regime shifts. They manage cross-strategy allocation, leverage limits, and enforce automated de-risking before stress events materialize.

Human-in-the-Loop Oversight (24/5): While execution is systematic, our dedicated human specialists provide continuous supervision over execution quality, slippage, and P&L patterns. A senior risk committee monitors tail-risk exposure and volatility responses, armed with defined emergency override protocols for black-swan events.

Infrastructure and Capital Buffers: Our ecosystem is fortified by redundant systems ensuring sub-millisecond latency. We mandate large liquidity buffers, highly conservative gross leverage limits, and high-frequency margin monitoring, supported by prime broker diversification to ensure continuous price discovery.

Global Footer / Call To Action